Given the amount of pushback that has come from the republican party, it seemed like it was only a matter of time before student loan payments started back up. Statements will go out in September with payments being expected in October.

This is already a bit more time than we were expecting given Sec. Miguel Cardona’s recent remarks, but it still is likely to cause many borrowers a lot of headaches.

While no one will be expected to pay back interest on all the time between the pause and now because at least Biden was willing to veto the cruel bill passed by Republicans and some Democrats, it is unclear exactly how much borrowers will be expected to pay back.

If you remember the original announcement from August of last year, one of the most important parts of the plan was a graduated repayment plan based on your income. Because the administration had to collect income to see if you qualified for any loan relief, they were also planning on capping the amount you paid at 5% of your monthly income, and the government would pay your interest.

At that point the big question was how many borrowers could the administration get to engage with the system, and even though millions applied for the month that the application was up, that is far from all of the people who would qualify.

So if they have your income information, will you still only have to pay 5% of your income?

It seems unlikely. Without a big push for income data from borrowers across the board, it seems unlikely that they will be providing even the bare minimum in terms of student loan relief.

It should be noted that there are still income repayment plans that can be negotiated with your lenders, and if you are in any danger of not being able to pay the loan amount in October, it is a good idea to do call them.

But those income driven repayment plans don’t waive interest. Interest simply piles up and piles up, increasing the principal of the loan every year. So if your income does eventually go up, so do your payments. It is an effective mechanism for trapping people with high student loan debt with that debt for the rest of their lives. Because no bankruptcy will discharge that debt, it will simply continue to grow for the lifetime of that person, and be taken out of whatever inheritance they manage to leave for any future generations.

Effectively keeping those least able to pay trapped in generational poverty.

Again, it is still a better idea than simply defaulting on the loans and failing to pay. They will not go anywhere and unlike credit card loans, they won’t be sold off for pennies on the dollar to collection agencies.

Getting people to engage in a simple online form was going to be difficult enough, but getting people to engage in the complex, demoralizing, and often compoundingly shameful act of asking for income driven repayment plans is going to be a hill that this administration is unlikely to cross.

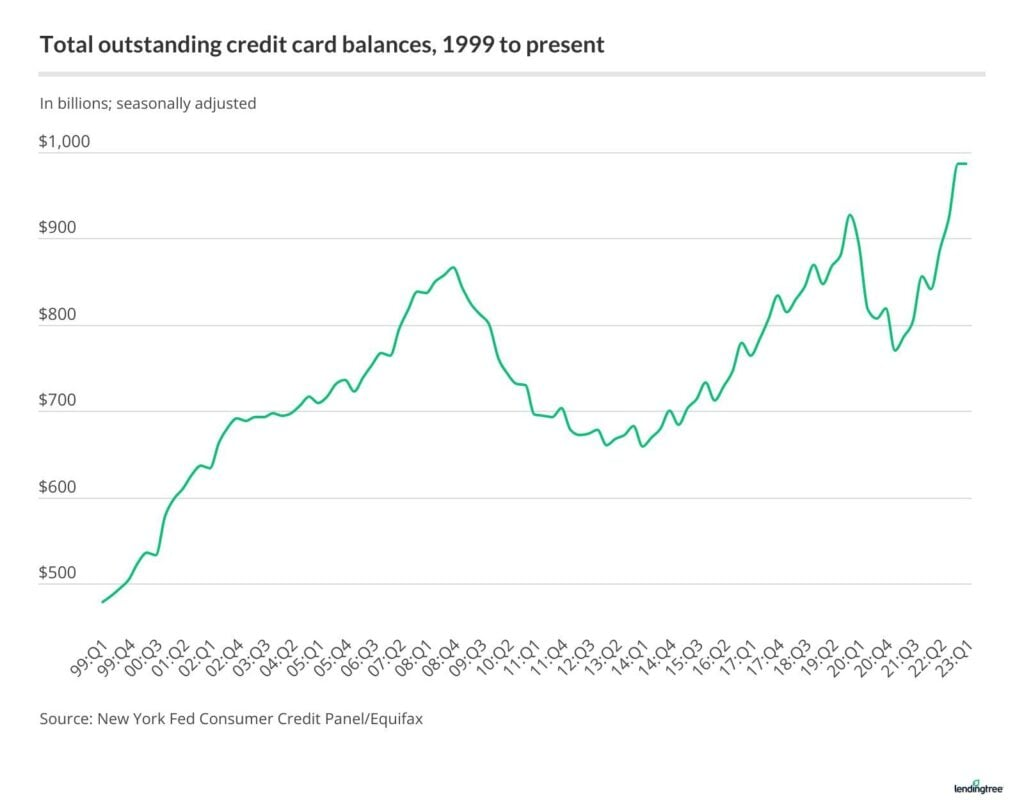

For a decade student loans have been seen as a financial bubble about to pop, and for the past three years, they have been in a holding pattern. When people have to make these payments they are likely going to take away from other, less crucial kinds of debt, especially credit card debt. And if you are unaware, credit card debt has recently hit an all time high.

So student loans might simply be a domino that topples all sorts of credit worthiness, and this could all come to a head during the election year.